A solo-built, AI-assisted tool for backtesting and simulating options strategies on historical data. A Python/FastAPI backend handles pricing and simulation; a Next.js frontend drives the research workflow. It is a research and analysis tool: it prices and evaluates strategies against historical data, and does not place trades, connect to a broker, or run live.

Pricing & Greeks

- Black-Scholes from scratch: hand-implemented option pricing and the full Greeks (delta, gamma, theta, vega, rho) rather than leaning on a library.

- Volatility models: historical and exponentially-weighted (EWM) volatility estimation.

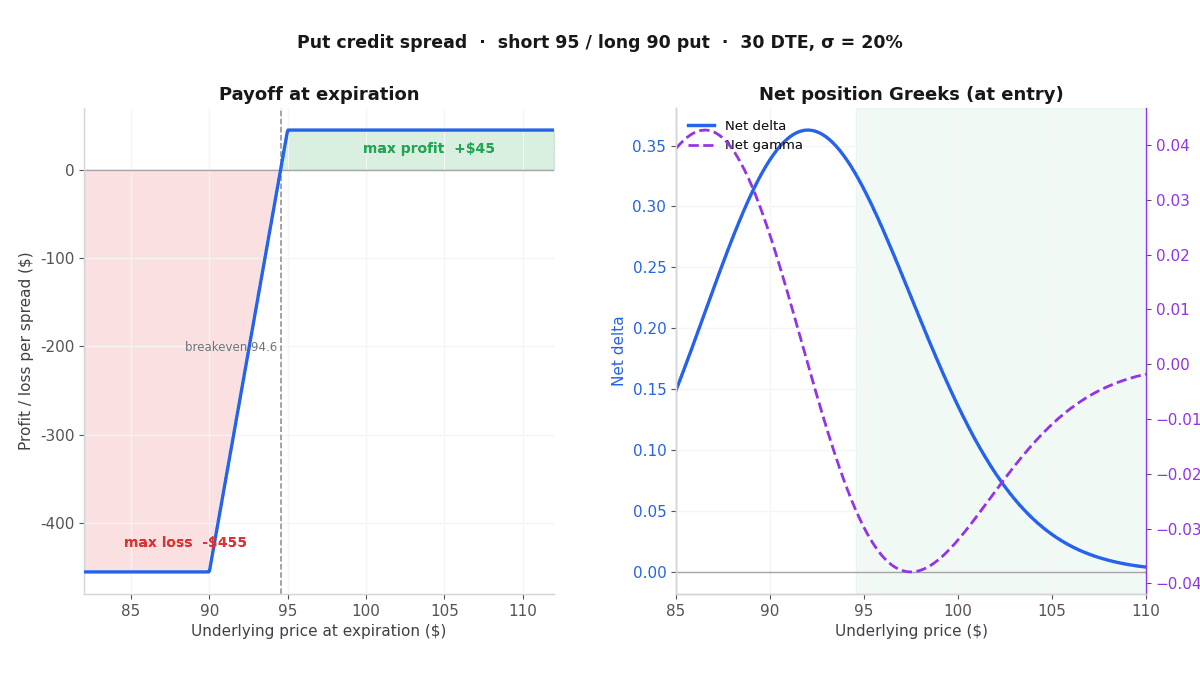

- Multi-leg spreads: pricing for put credit spreads, iron condors, and calendar spreads.

Quant validation

Strategies are evaluated across a 25-ticker universe over 10+ years of historical data, with a research log spanning a dozen experiments. The layer that keeps those results trustworthy rather than just plausible:

- Walk-forward, out-of-sample testing so strategies are judged on data they were not tuned on.

- Bootstrap resampling for confidence intervals around performance estimates.

- A/B testing with Fisher's exact test to compare strategies statistically.

- Explicit look-ahead-bias and survivorship-bias controls to keep backtests honest.

Engineering

- An extensible

PricingProviderabstraction, so pricing sources and models can be swapped without touching strategy code. - 21 test files covering the pricing and simulation core.